Want to Avoid Business Jeopardy? Focus Only on This

Do you want to avoid any kind of business problems, especially bankruptcy? If you can secure this one thing – focus on only this – your survival rate surges dramatically: Making cash from operations. That’s it. Even if you are good at sales or making the best product, if you can’t secure cash from operations, your business will eventually die.

Without cash from operations, you’ll keep losing money until your business dies. You can’t pay debt without operational cash flow – that’s bankruptcy. Having cash flow from operations increases your chances of successful refinancing, even if you can’t pay everything.

So make sure your new cash allocation certainly generates cash from operations. You don’t have to jump before you know the situation – jumping after things become clear still works.

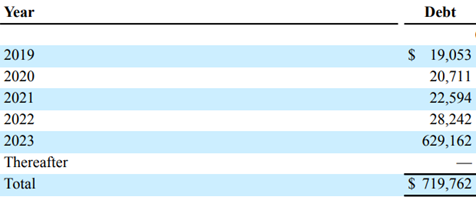

I want to introduce a new case study of this kind of bankruptcy story. Ebix is a software company that develops software on demand. This 47-year-old company went bankrupt in 2023. The direct cause was its inability to repay $600M in debt in 2023. All of that $600M debt came due in the same year, 2023.

[From EBIX-2018-10K p95]

Very funny. Why such an arrangement? Like teenagers who think they’ll be billionaires in 5 years, so they’ll have no problem paying all the borrowed cash at once. Worse still, even when it became apparent they couldn’t pay the debt, they kept acquiring new companies and paying dividends.

Their profit-and-sales-first mindset killed the company. Profit increases even if they buy a business for 1000 but only make a profit of 10 annually. In this case, profit is only +10, but the cash outflow is a significant -1000. Maybe sales increase by 1000, but if the profit increase is only 10, that is nothing.

This company historically increased sales by buying small companies. The big purchases were in 2017 (two $70M companies) and in 2018 (an Indian foreign exchange company for $170M). Those were bought with borrowed cash, so debt increased rapidly.

They had to accumulate cash to repay the debt, especially in 2023 when they had to pay $629M. Their operating cash flow in 2018 was around $80M, and they had to pay capital expenditures like buying equipment and other fixed assets to maintain operations (about -$10M a year). Debt payments were around -$20M a year, so they could make only $50M in cash per year, if everything went without troubles. They could accumulate only $250M in 5 years, and with what they had in 2018 in cash ($180M), it would add up to $430M – not enough to pay the debt in 2023. So they had to either generate more cash somehow or hopefully get refinancing when the due date came.

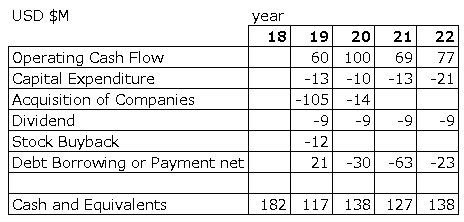

Here is what happened after that. Look at the cash flow matrix below.

By the end of 2022, they only had $138M, far from even the $430M estimated. Looking at this situation, banks refused to refinance the company, letting it die.

I want to share my thoughts on the situation:

- In 2019, they acquired another company for $105M. Everyone thought they were done with acquisitions, but they went ahead and bought another company anyway. And with dividends and stock buybacks – they didn’t have that cash to spend, they needed to accumulate it for debt repayment, but they kept spending. This shows there must have been no cash flow management, which leads to my next point.

- I’m certain the CEO didn’t even create this simple cash flow matrix shown above. Maybe the company made it when presenting to banks, but I bet the CEO just ignored it. I imagine the CEO’s attitude was like “Cash flow? That’s worthless trash – increasing sales will solve all problems.” That’s a dangerous attitude. Always make cash flow planning matrices!

- They were overly optimistic. This company had increased sales and profits through company acquisitions in the past, which led to a five-fold stock surge from 2014 to 2016. So they thought, “Why wouldn’t the same thing happen this time?” They assumed the newly acquired companies would bring profit and cash would flow naturally.

- Here’s a really mysterious use of their brain: they bought companies – maybe many of them were loss-making companies or negative cash flow companies. Those acquired companies didn’t contribute to future cash generation, only increasing useless stupid sales figures. They must not have understood that investment is about generating cash, not just increasing sales or even profit.

- When you buy additional businesses, yearly capital expenditure increases because operations expand. This is very normal, as you now have more business to maintain. You have to buy more fixed assets in the future. In this case, not only did business operations fail to generate cash, but they required increased capital expenditure.

To sum up, underestimating cash flow will kill your company. Having even a simple cash flow planning matrix is much better than having none at all.