Why SaaS CAC Calculations Fail And How to Fix It

For every SaaS company, calculating Customer Acquisition Cost (CAC) is critical. Companies track this metric as one of the most important, but often calculate it wrong. There are many hidden challenges that make calculating CAC difficult.

When you calculate CAC wrong, it leads to flawed strategic decisions based on incorrect numbers, resulting in completely wrong business choices that can harm your company. To avoid this, today I (CPA) will explain what makes CAC calculation so challenging and how to calculate it correctly.

Reason 1: Failure to Track Time Properly

The foundation of accurate CAC calculation is tracking the time of all employees, including the business owner. In small companies, one person often wears multiple hats, which creates a chaotic situation. When one person handles sales, marketing, and customer success simultaneously, how do you allocate their labor costs appropriately?

If you want to calculate CAC accurately, the first step is to record employee time correctly. You need to know how much time they spend on each specific task (such as email marketing within the marketing function), which product they’re working on, and which customer tier they’re targeting.

Without this information, you’ll never know your true CAC. Everyone, including you, must participate in time tracking. Unfortunately, employees often don’t understand the importance of time tracking. They tend to record random hours, thinking, “I’m actually working on tasks that matter. Time recording is just a waste of time, but my boss insists, so I’m doing it reluctantly.”

You must communicate to employees that their time recording is the basis of CAC calculation and represents very important data. If they don’t record time correctly, the company will make wrong decisions based on incorrect numbers, which can have serious consequences.

Reason 2: Inability to Track Non-Measurable Marketing Activities

All advertising costs and results must be trackable. However, what happens when you’re running ads where you can’t track the results, like a Coca-Cola commercial on TV?

The answer is simple: Don’t do that. Always choose ads where you can track the ROI. Avoid advertisements that only increase brand recognition without measurable outcomes. Your content must create leads, your email marketing should always sell something or invite people to webinars, and webinars should sell them something too—not just provide information without any call to action.

Reason 3: Executive and Manager Cost Allocation

This is a tricky part. How do you handle costs like the salary of a Sales Vice President? Many SaaS companies don’t know how to deal with this, so they simply exclude it from CAC calculations.

Actually, this approach is often appropriate. A VP’s job is primarily strategic thinking, and their costs are fixed expenses. Even when sales increase, these costs remain the same (unless you need multiple VPs).

The reasons you want to calculate CAC are:

- To compare channel costs and find the most effective one

- To compare it with Customer Lifetime Value (LTV)

- To see long-term growth through simulations

- To determine the profitability of each customer tier

- To compare this quarter’s efficiency with past performance

Understanding Fixed vs. Variable Costs

If you change VPs frequently, or the number of VPs and their salaries vary often, you might want to include VP labor costs in your CAC calculation. However, if these costs are stable, you don’t need to forcefully allocate VP costs to CAC.

Only when comparing CAC to LTV (Reason 2) might you want to include all costs, including fixed costs, in your CAC calculation. For instance, if your CAC, including fixed costs like VP salary, is $100 and LTV is only $90. Is the business doomed? Actually, it’s not. Economies of scale (higher sales volumes dilute fixed costs per unit sold) apply as you grow and decrease your overall CAC.

For example, if you acquire 100 users this year, paying $1 in ads per customer. And $1,000 to a VP as salary, simply dividing the VP cost by units sold gives you a CAC of $11 ($1 + $1,000/100). When you get 1,000 customers, the CAC becomes $2 ($1 + $1,000/1,000). The acquisition efficiency doesn’t change—it stays at $1 per customer—but increased sales volume results in a seemingly 5x lower CAC. What’s the point of this calculation?

It’s hard to imagine situations where you must allocate VP costs into CAC calculations. Moreover, it’s difficult to allocate in real situations. If you’re selling products A and B, how can you allocate VP costs when they’re making strategy rather than doing direct work?

When to Include Manager Costs

When calculating sales manager costs, however, you should include them in CAC. These costs increase as sales increase. For example, if your sales manager supervises 5 sales reps and you add 5 more reps, you’ll need another manager. Even though managers don’t sell directly, you should include their costs in CAC calculations to see the true efficiency of your customer acquisition efforts.

Practical Manager Cost Allocation Example

Cost allocation for managers is somewhat tricky because they don’t do direct work. (This is where boring calculation starts. You can skip to Reason 4 if you don’t want to know the details.)

Here’s a simple example: You’re selling one product with two tiers (mid-sized and enterprise). One manager supervises two reps. The first rep worked 100 hours for the mid-sized tier and 200 hours for the enterprise tier with a $3,000 salary. The second rep worked 200 hours for the mid-sized tier and 200 hours for the enterprise tier with a $5,000 salary. The manager’s salary is $10,000.

You can allocate this by the costs of reps’ direct time. More precisely:

- Mid-tier cost: (100/300 × $3,000) + (200/400 × $5,000) = $3,500

- Enterprise tier cost: (200/300 × $3,000) + (200/400 × $5,000) = $4,500

Therefore, manager cost allocation is:

- Mid-tier: $10,000 × ($3,500/$8,000) = $4,375

- Enterprise tier: $10,000 × ($4,500/$8,000) = $5,625

You then add these allocated costs to each tier’s CAC calculation.

Reason 4: Failure to Track Long-Term Customer Journeys

Especially for larger customers, it takes a long time with multiple touchpoints to convert them into paying customers. Many companies fail to follow their conversion journey throughout this extended period.

You must track each customer through all steps. When and where did the customer initially come from? All records are needed to properly allocate costs. This data tracking requirement leads directly to our next reason.

Reason 5: Don’t Know What Cost Allocation Is

This is the biggest cause of difficulty in CAC calculation. First, you must understand there are direct costs and indirect costs.

Direct costs are expenses that can be directly tied to a specific product, customer tier, or activity. Indirect costs are shared across multiple products, customer tiers, or activities and cannot be easily attributed to any single one.

Direct costs are straightforward. For example, a sales rep’s time spent selling Product A to SMB (small business) tier customers. You can easily calculate this cost by dividing their salary by the time spent on this specific job.

Indirect costs, however, are much trickier. For instance, your marketing team writes blog articles that generate leads across all customer segments from SMB to enterprise. Also, you can’t identify which specific article convinced someone to convert into a lead. This is an indirect cost. Most people either ignore these costs when calculating CAC or simply divide yearly marketers’ labor costs by the total number of customer acquisitions. Both approaches are far from accurate.

Basically, proper CAC calculation requires cost accounting knowledge, which most SaaS company CEOs don’t have.

Calculating Costs at Each Touchpoint

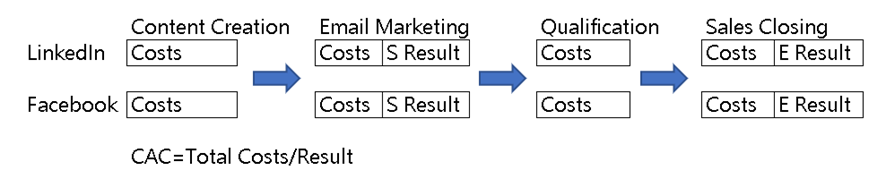

You need to calculate costs at each touchpoint. Here’s a simple example: Your target is both SMB and enterprise customers, and you only sell one product. You’re marketing on LinkedIn and Facebook. Both channels bring readers to a landing page and generate leads. Then you implement email marketing. Enterprise customers typically require sales qualification and closing, while SMBs are self-service.

(S Result is how many paid SMB customers you acquire this time; E Result is how many enterprises you close through sales this time.)

The key is to horizontally add up all costs and get the total cost of each channel. Then divide it by the result (paid conversions) from that channel.

The Complexity of Content Cost Allocation

Let’s look at content creation costs. Suppose the CEO creates content with a $200,000 salary and 2,000 work hours annually. The labor cost per hour is $100. If you spend 100 hours on LinkedIn content creation, that’s $10,000 in labor costs. How do you allocate this to each tier’s CAC?

If content brings 100 enterprise and 1 SMB lead, is allocating 50% of costs to each tier rational? No, this content clearly targets enterprises; most costs should be allocated to the enterprise tier CAC.

Similarly, if content brings 100 enterprise and 100 SMB leads, but enterprise LTV is 100x bigger than SMB, should you allocate costs equally (50% to each)? No! The value of enterprise customers is 100 times greater. In this case, SMB leads are just a small bonus, even if the lead numbers are equal.

That’s why costs should be allocated by result numbers × LTV ratio:

- Enterprise: 100 leads × $100 LTV

- SMB: 100 leads × $1 LTV

If you spent $10,000, the cost allocation is:

- Enterprise: $10,000 × (100 leads × $100 LTV) / ((100 leads × $100 LTV) + (100 leads × $1 LTV)) = $9,900

- SMB: $10,000 × (100 leads × $1 LTV) / ((100 leads × $100 LTV) + (100 leads × $1 LTV)) = $100

Of course, there can be direct labor hours too. If you spend 5 hours writing only for SMB, the cost would be: 5 hours × $100 + allocated indirect labor costs.

Sales Cost Allocation is Simpler

On the other hand, sales costs mainly consist of direct costs, making them easier to calculate. You can track exactly how much time sales reps spend on each tier or even specific customers. You calculate CAC by dividing labor costs by conversion results.

Putting It All Together

Finally, add up all costs from each touchpoint of a specific channel, and then you can determine which channel is most efficient for customer acquisition.

Conclusion

Proper CAC calculation requires understanding both direct and indirect costs, tracking customer journeys across all touchpoints, and applying appropriate cost allocation methods based on customer tier and lifetime value. Only with accurate CAC calculations can SaaS companies make informed strategic decisions about their growth investments.