Make Losses Forever vs Turn Profitable: This is the Difference

In 2023, the workspace renter WeWork went bankrupt. The company, once valued at $47 billion, plunged to zero. When investors were excited by WeWork, they saw it as an IT high tech company. Then everyone thought “Nah, it isn’t”, and the stock dropped. To me, that is quite natural. Everyone knows that their business is not profitable. Every new workspace it creates operates at a loss.

WeWork’s business structure is not an IT company’s at all. It is more like airline companies.

Normally, when an IT company’s sales volume increases, the cost decreases. For example, a tech company like Netflix, once they make a video, whether there are 100 viewers or 1 million viewers doesn’t change the cost. Suppose it takes $1 million to make a video, if there are only 100 viewers, the cost per client is $10 thousand. But if there are 1 million viewers, the cost decreases to only $1.

This is called “economies of scale.” The content is called intangible assets, like software. This kind of company operates at a loss at first, but when the user base increases, it generates tons of profit because the sales increase but the costs don’t. Another example is car companies. It costs a lot initially because they have to invest heavily in manufacturing plants, machines, design, employee training, etc. But after they make these and increase the production, the cost per car reduces significantly, like Netflix content. And if they buy materials in bulk, they can get a discount. This is called economies of scale.

On the other hand, WeWork can’t have those advantages. Airline companies are unlike IT companies; they can’t get economies of scale. When airplane capacity is full, they have to buy new ones. They can’t put travelers in already full airplanes to reduce cost per client.

A bigger scale doesn’t decrease the cost. If it is an IT company, it doesn’t matter if there are 100 or even 1 billion users, all users can use one software simultaneously.

WeWork declared it is a ‘tech’ company because it uses computer-aided design (CAD) when it makes the new workspace (who doesn’t?). Also, it is ‘We’ Work, which means they wanted to transform a workplace into a community like Facebook, not just a place where a bunch of strangers work. That is why they say it is ‘very different’ from a normal workspace. Turns out no differences.

If one workspace operates at a loss, increasing the number of places doesn’t make it profitable. Each space has its capacity limitation. Unlike other tech businesses, if WeWork keeps putting customers in the same workplace, the place gets so crowded that it becomes hell. So they have to make a new workspace to get more customers.

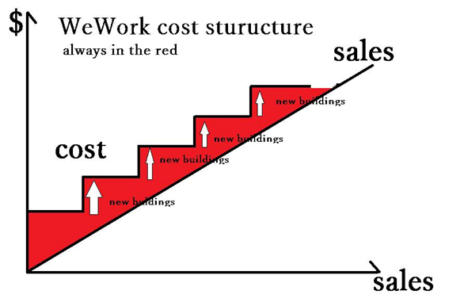

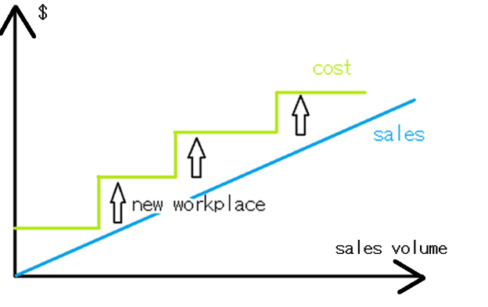

That is why this situation lasts forever. As you see, selling more doesn’t solve the WeWork problem at all. Its costs don’t reduce even if it gets a lot more clients. The cost structure of WeWork is like the graph below.

When it makes a new place, a new cost occurs (like renting a new building, buying equipment…), then the costs become stable with sales increase to some point, but when it goes over capacity they make a new one, and the additional cost occurs again. The costs always exceed the sales, making it an eternally loss-making company.

Of course, the company should generate positive profit and cash flow from every workplace it operates.

The reason its costs always exceed sales is that WeWork always rents the best buildings in the biggest cities, and they expand users rapidly with extensive advertising. WeWork’s monthly fees charged to clients are high, but not high enough to cover those costs. They spent advertising fees, but members kept quitting, and ad fees became operational costs, to just retain the customer number the same each year.

It is not an investment for the future. Great advertisement investment for the future is like this: You spend the ads fee, and it acquires a new customer who not only stays for very long but also brings their friends to the company. Clients become great assets for the company’s future growth.

That actually happens to companies like Snowflake or Slack. Their sales retention rate exceeded 100%, which means customers not only stayed but also brought new clients like the same company’s different divisions.

WeWork’s unique selling proposition (USP) is providing great buildings at great locations. All their workplaces are in the best of the best buildings. However, that actually doesn’t solve the user’s problem so they can only charge a monthly fee less than what it takes, and get a very low retention rate.

Masayoshi Son, CEO of investment company Softbank was the biggest investor in WeWork. WeWork could operate with a huge loss because of his deep pocket. When WeWork got into cash trouble, he paid.

He was once a golden god investor. Everyone respected him, thinking he was a true genius. He invested in Alibaba from an early stage and made tons of money. He really likes things that grow fast, like a cat loving fast-moving mouse.

And he invested more than $10B to bail out WeWork, it was really stupid. He paid insanely high for the loss-making trash (no offense).

People tend to do insane things when they become billionaires. Like Elon’s Twitter buyout and Zuck’s metaverse investment.

Don’t invest in a business unless you can calculate when and how much the profit and cash flow will be, and ensure that they will exceed the initial investment.