Profitable, But Where Is the Cash? Avis case

Have you ever wondered why some companies report profits year after year, yet struggle to keep cash in their coffers? This paradox is more common than you might think, and it’s a crucial issue in today’s business world.

Many companies are profitable, while their cash flow is always negative. Why? The answer lies in the nature of business operations. These companies often require escalated investment constantly, like buying new machines to make better products. But here’s the catch: their competitors are doing the same thing. As a result, they can’t increase their selling prices and never truly reap the rewards from their investments. Just to stay competitive, they have to spend much more than their profit.

Understanding Free Cash Flow

To grasp this concept fully, we need to understand what free cash flow is. Simply put, free cash flow is operating cash flow minus capital expenditure (the purchase amount of fixed assets like equipment). This is literally the cash you can use freely, like paying back debt, paying dividends, or buying whatever you want.

Here’s a key point to remember: a company’s ultimate goal is to maximize free cash flow, not to increase sales or profit. You might be surprised to learn that the majority of financial analysts value companies using DCF (Discounted Cash Flow). In simple terms, this method regards the total future free cash flow as the company’s true value.

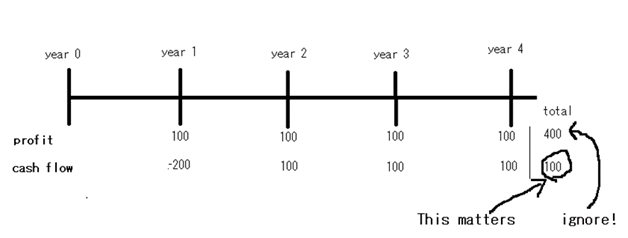

Let’s look at an example:

In this case, even though the company reports total profits of 400 but this doesn’t matter, its total value is based on future cash flows which is only 100.

The Profit-Cash Flow Deviation: A Case Study of Avis

To illustrate this concept, let’s examine Avis, the biggest car rental company in the US. At first glance, Avis seems to have it all. It’s the industry leader, which should build trust among customers. But here’s the catch: being No.1 doesn’t necessarily mean higher profits or better cash flow. Why? Let’s break it down.

In the rental car business, economies of scale don’t work as you might expect. This is because each car can only be used by one group each day. Economies of scale typically involve using one asset more and reducing the per-unit cost, but it doesn’t work in this case because a car can serve only one customer at a time.

Even the biggest car fleet doesn’t significantly reduce the car cost. Avis does get a small discount when buying cars in bulk, but that’s about it.

The Business of Car Rental Economics

To understand a car rental company’s profitability, we need to look at three key factors:

- Rental prices

- Used car prices

- New car prices

These factors affect both revenue and costs in interesting ways:

- When rental prices go up, it’s good for sales and increases profit, and vice versa.

- When used car prices are high, companies can sell their old cars for more money, which reduces their depreciation costs and boosts profits. (In the rental car industry, it’s customary that the price of sold cars is deducted from depreciation cost.)

- When new car prices go up, depreciation costs increase, which is bad for the bottom line.

The Covid Profit Bonanza

The car rental industry experienced a rollercoaster ride during and after the Covid-19 pandemic. Here’s what happened:

- Rental prices went up due to increased demand.

- Used car prices skyrocketed, allowing rental companies to sell their old cars for much higher prices.

- New car prices also increased, but the increase was mild compared to the used car price surge.

These factors led to a temporary boost in profits. That’s why this company was so profitable in recent years.

But here’s the twist: investors aren’t convinced this good fortune will last. They’re expecting rental prices and used car prices to drop, which would hit profits hard.

This skepticism is reflected in Avis’s valuation. In April 2024, Avis had a price-to-earnings ratio (PER) of just 3, making it one of the cheapest stocks in the US. This low valuation tells us that investors are worried about the company’s future.

They Earned Much Profit, So Why Did They Lose So Much Cash?

Now we come to the heart of our paradox. The company was profitable in recent years, so where has all the cash gone? There are two main reasons:

- Escalation of inventory level

- Very aggressive stock buybacks

Let’s dive deeper into each of these factors:

1. Inventory Escalation

In the past 10 years, Avis’s total net income was $6 billion, but the total free cash flow was negative, -$2 billion. That’s a significant difference!

The main reason for this deviation comes from the inflated vehicle prices on the balance sheet. When they increase car possession, they have to put cash into it, reducing available cash. The car purchase amount doesn’t become a cost immediately; the cost occurs through depreciation over time. That’s why profit and free cash flow deviate.

But why was the car amount inflated to twice the size, from $12 billion in 2019 to $21 billion in 2023? The primary reason is car price increases. Over the last decade, new car prices have increased due to inflation, especially during the Covid era.

What’s more concerning is that new car prices seem unlikely to go down in the future. This situation may last not just for 2-3 years but potentially forever. As inflation keeps increasing car prices, this company might never achieve positive free cash flow in the future.

Remember what I said about company valuation earlier? Since company value is decided by DCF, if free cash flow is negative, the company’s value is less than 0. That’s the second reason why the company’s stock is so cheap compared to its reported profits.

2. Aggressive Stock Buybacks

Avis has repurchased its own stocks at an insane speed since 2014. The total stock amount is down from 105 million in 2014 to 35 million in 2023. This means that if the profit is the same every year, each stockholder’s share of the profit has increased from 1 to 3, even if the total profit remains unchanged.

However, there’s a significant downside to this strategy. As a result of the huge stock buyback, the company’s debt increased from $11 billion at the end of 2020 to $23 billion at the end of 2023.

Stock buybacks can be great if the company stays alive and generates substantial free cash flow in the future. But they have to pay back the debt eventually, which will reduce future cash flow.

And this huge debt combined with low free cash flow makes it difficult to refinance. Banks may not be willing to lend cash again. So if they have no cash to repay the debt when it comes due, it might spell the end of the company.

In conclusion, Avis’s story serves as a cautionary tale about the difference between profitability and cash flow. It highlights the importance of looking beyond headline profit figures to understand a company’s true financial health. As investors and business analysts, we must always remember: cash is king, and free cash flow is the lifeblood of any sustainable business.