Good USP Bad USP: How to Make a USP That Works? Netflix case

On April 20, 2022, Netflix stock dropped 35% in a day, from $348 to $226. The stock price kept dropping to reach half of the original price in a month, which was $170. A significant drop from October 2021’s high of $690.

There were some reasons for that.

That day was the quarterly financial release day. And 1. the number of subscribers decreased for the first time in a decade. Netflix had reached maturity, investors thought there would be no more growth. 2. The tech industry got hit hard because of the recession risk. 3. The competition was getting harder, the streaming service industry was too crowded, and Netflix would have to cut the subscription price and increase content to compete with others, which would lead to less profit. 4. COVID was ending, people would not stay home anymore, and investors thought people wouldn’t watch videos inside their houses.

It turns out all of these were wrong. Netflix’s sales and the number of subscribers are still growing (but slowly). The recession never happened. Netflix didn’t cut the subscription fee; on the contrary, it raised the fee by 20% in the US, I will explain this later. In the post-COVID era, people are still using streaming services.

The stock price went back to $600, although it took close to 2 years after the crash.

Netflix’s growth speed decreased significantly after the stock drop. Before 2020, the average sales growth was 30%, but in 2021, it went down to 18%. Then the first subscription drop occurred in 2022, then the growth rate dropped to 6%. In 2023, the growth rate was still 6%. The company is not the same company as before.

Now the stock price is around $550 (April 2024), and the PER (price-earning ratio) is around 40. That means the stock price is 40 times higher than the profit per share. It is too high for a slow-growing company.

This high PER shows that investors still believe this company will invent something new in the future and draw a new growth curve again like it did in the past. This company evolved from an online DVD rental service to a streaming service, and then to an original video creator. When the situation changes, it evolves itself and its USP.

Let’s see its USP.

USP: once a video streaming service itself was a huge USP because nobody else provided that. At the time, they had to go to video rental shops to watch movies in their houses. And a streaming service solved those problems. People were bored and wanted to have some fun, but going out and renting videos was tiring. And of course, they had to return it to the rental shop; they were often late for the deadline and had to pay an additional fee for that. Only Netflix provided the solution for the problem: streaming service.

But now things have changed. So many streaming providers (Apple TV, Amazon Prime, Hulu, Disney+…). When a situation changes, the former USP no longer works as a USP. Every other platform is streaming videos. To stay a profitable company, Netflix had to find another USP to survive. Their streaming apps are almost identical, so Netflix has to differentiate with their original content.

Right now, the target is people who are curious about what’s in now. They like watching the latest dramas and movies. They like to talk about those shows, and they think knowing about what is hot right now makes them interesting and cool.

Certain mega-hit titles are only on Netflix, so they subscribe to Netflix.

The USP of Netflix is now that they can constantly make big hits that people talk about. Netflix’s strategy is like venture capital’s. They invest in a wide variety of content, and the majority of it just fails, but very few become mega-hits, compensating for all the losses the failed content made. Netflix also doesn’t know what will hit, so they have the largest portfolio of original content, and some of them became smash hits like Squid Game or Stranger Things.

Netflix’s 61% of content is now original content. And speaking of original content, the biggest rival Amazon Prime’s original content, no one can name even one title.

Let’s see how this USP affects its accounting.

First, you can see the huge content assets on a BS (Balance Sheet). It was $31.6B (billion) in 2023. Total assets were $48.7B, so 65% of all assets were content. This is because if they don’t possess that big content, it can’t act like venture capital as I said. Licensed content was $12.7B, and original content was $19B.

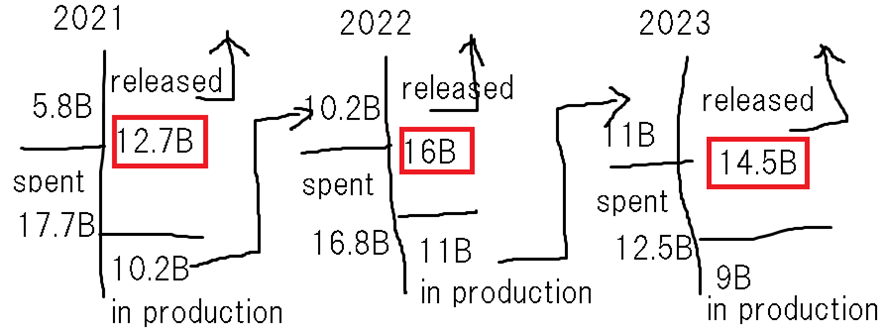

The important thing is how much they spend on content. Netflix spent $12.5B on content in 2023. This seems much fewer than the last 2 years. In 2022, it was 16.8B, and in 2021, it was 17.7B (from the Cash Flow Statement). It seems they have less content now.

Now, here’s the tricky part: Not all of the $17.7 Billion spent went to releasing new content in 2021. Some of it was added to the “content in production” that hasn’t been released yet.

“Content in production” refers to the content that is currently being made but has not yet been released.

As you can see, in 2021:

They started with $5.8B content in production.

They spent $17.7B on content.

They ended with $10.2B content in production.

The released content value is calculated as $12.7B.

A simple example of this is, if you had 5 dollars in the morning, then you got 17 dollars as a salary, then you used some of it, and you saw your wallet, there were 10 dollars in it, how much did you use today? Answer: 12 (now x is the spent amount, 5+17-x=10, x=5+17-10, x=12)

In 2022, the release amount was 16B, and in 2023, 14.5B.

So the claim that Netflix is reducing product release is very wrong.

While competition got harsh, the streaming service raised its price in 2023. That’s weird.

In the EV industry, when competition got too harsh, they cut prices. In the streaming service industry, the opposite thing happened. This situation is explained only by this: In the streaming industry, each service is differentiated by its unique content. This means that even though they are in the same industry, they aren’t direct substitutes for each other. For example, if you want to watch a particular show that’s exclusive to Netflix, you can’t switch to Disney+ or HBO Max for that show. This gives streaming services some power to raise prices without losing their customers.

They subscribe to Netflix because they have certain titles to watch. The result is a little bit counterintuitive, but the numbers (the price hike without decreasing paid customers) say so.

And its USP, creating a huge amount of original content, is supporting this price up.

On the other hand, in the EV industry, while there are differences between each car, they are all substitutes for each other to a greater extent. If the price of a Tesla goes up, you might buy a Ford or a Toyota instead. This is because EV cars bring identical merits to the driver. This competitive pressure led to price decreases.