This One Big Idea Will Make Your Business Cash Rich, and You’ll Never Worry About Payments Again

The Cash Flow Paradox: As Sales Grow, Cash Decreases

When sales increase, you might suffer from cash shortages. The more sales, the less cash. Sounds counterintuitive?

When sales increase, mainly two cash outflows increase: capital expenditure and working capital. Capital expenditure is when you buy machines or property to address increased sales volume. Working capital is about putting your cash into operations. For example, when sales double, you have to prepare twice the size of inventory, so you have to put twice the amount of cash into inventory.

Introducing the Cash Conversion Cycle (CCC)

Let me introduce you to the CCC (Cash Conversion Cycle). CCC reveals how fast products on your shelves become cash in hand. This also shows how much more working capital is required when sales increase.

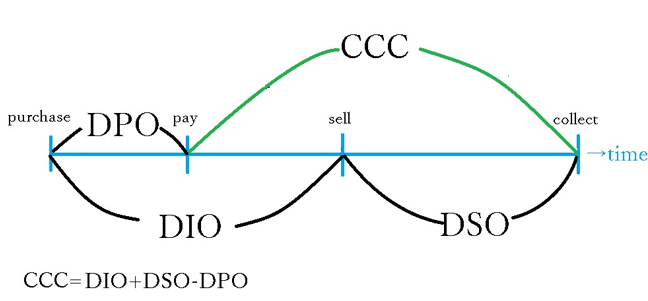

Look at the diagram below:

Ignore DPO, DSO and DIO, just focus on CCC. CCC is the period from purchase payment to receivable collection. The shorter it is, the better, because it means the company can retrieve cash faster.

For example, if you buy flowers from a wholesaler and pay immediately on Aug 16th, then sell the flowers on Aug 20th and get paid immediately, the CCC is 4 days. 4 days is very short, so it’s good for your business.

For a typical company, CCC can easily exceed 6 months because collecting receivables (when you sell the product but receive the payment later) takes longer.

Components of CCC

The period between selling the product and collecting the receivable is called DSO. And when DSO gets longer, CCC also gets longer. You can see this in the diagram.

You can calculate CCC with this formula: CCC = DIO + DSO – DPO. It’s obvious if you check the diagram.

Each period represents:

- DIO: from purchase to sale

- DSO: from sale to collection

- DPO: from purchase to payment

Your goal is to minimize the CCC to minimize the working capital (the cash you have to put into your operation). Cash shortage problems often occur because a lot of cash is tied up in working capital.

Why does a shorter CCC mean less working capital? Suppose you sell $100 each month. For simplicity let’s say you buy the product for $100 and sell it for $100. When CCC is 1 month, you purchase a $100 product, sell it, and then collect the money 1 month after purchase. So the $100 is tied up in working capital.

If CCC is 4 months, you have to buy $100 of inventory to sell in the first month, then another $100 purchase the next month, and so on. After you’ve put in a total of $400, you finally receive the first month’s sales price of $100. This is why a longer CCC requires more working capital.

How to calculate DIO, DSO, and DPO?

- DIO = (inventory ÷ sales) × 12 months

- DSO = (receivables ÷ sales) × 12 months

- DPO = (payables ÷ sales) × 12 months

For example, suppose you have $100 worth of flower inventory at the beginning of the year, and your total sales this year were $10,000. This means you sold a $100 inventory 100 times ($10,000 ÷ $100) in a year, so it takes only 3.6 days (365 ÷ 100) from purchase to sale. This is the definition of DIO. DIO can also be calculated using the formula: ($100 ÷ $10,000) × 12 months = 0.12 months = 3.6 days. You can calculate DSO and DPO in the same way.

How to calculate working capital increase when sales increase?

sales increase per month × CCC

For example, a CCC of 4 months means you have to put 4 months’ worth of sales into working capital. Remember the first case where you put $400 as working capital? That’s worth 4 months of sales. When sales increase to $200/month, it takes 4 months to retrieve it, so $200 × 4 months = $800 is needed. The original was $400, so there’s an increase in working capital of $400.

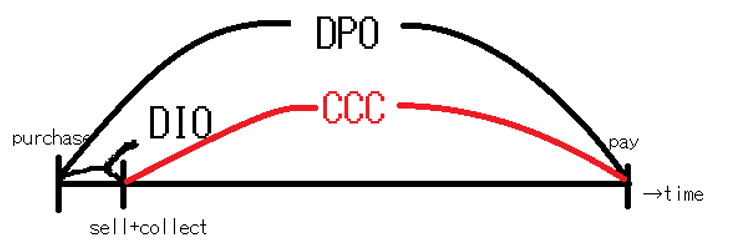

The extreme case: negative CCC

Here’s what I wanted to highlight: there’s a Chinese EV car maker called Li Auto, one of the biggest EV car makers, and Li’s CCC was -4.3 months in 2023. Negative CCC does exist. Look at the diagram below. You first get sales cash, then 4 months later you pay for the purchase of materials, etc. You’ll never experience a cash shortage from operations like that, even when sales increase rapidly.

On the contrary, this company’s cash from operations will increase when sales volume increases.

In 2023, DIO was 0.6 months, DSO was almost 0, and DPO was 5 months.

This happens when the company has power over the supplier, so the company can delay the payment timing. Li can collect the cash way before paying for the purchase (like windows, batteries, or steel).

Providing benefits to suppliers is key for extending DPO. For example, if you have a strong balance sheet and good reputation, suppliers don’t have to worry about uncollectible situations.

Shortening DIO and DSO is also important to achieve negative CCC. If you minimize inventory, DIO reduces. And if you get paid even before you provide a service or product, DSO becomes much shorter and operations require much less cash.

From Li’s cash flow statement, we can see it actually gets cash from the negative CCC. Operating cash flow increased in 2023 by $7.1 billion. The main cause of the increase was an increase in trade and notes payable by $4.4 billion. Rapid sales growth from $6 billion in 2022 to $17 billion in 2023 and negative CCC due to long DPO increased cash flow.

How a negative CCC generates cash: an example

Suppose you sell $1 billion/month and DPO is 4 months. For simplicity, let’s say DIO and DSO are 0, and material prices equal sales price.

The first month, you get $1 billion in sales cash, but you don’t pay the material costs. You accumulate $4 billion in cash, then finally pay $1 billion (at the same time, you receive this month’s $1 billion sales cash). So now you have a $4 billion cash pool. This is the negative CCC cash creation magic.

You can use this cash for whatever you want. Even if you lose all the 4 months’ cash pool, your company can still operate because this cash pool never dries up, as long as you continue the operation and sales don’t decrease. When you pay for the monthly purchase from 4 months before, you get new sales cash this month.

Negative CCC increases cash flow from operations when sales grow. On the contrary, positive CCC decreases cash flow from operations when sales grow. This is the biggest trap for many fast-growing ventures. Sales are increasing, but the cash amount becomes less and less. What’s happening? Answer: positive CCC. It eats up all the cash it has.

I want you to aim not only for 0 CCC but beyond, for negative CCC.