Are You Selling a Good Thing as a Cheap Commodity? Focus on Your Strong Point!

Krispy Kreme is selling donuts. It has a long history, and the iconic donut is loved by Americans as a good old style. The donut is airy and has a thick sugar coating all over it.

Since its IPO in 2000, Krispy’s sales and profits increased every year like crazy. The sales increased more than 3 times in 4 years.

However, in fiscal 2004 (ending Jan 2005) the company’s sales per store (which the company owns) suddenly dropped 13%. This is a stable business, that seems very abnormal.

A famous marketer once said, “When carb reduce diet craze kicked in, people no longer bought sweets, which caused a decrease in sales for Krispy Kreme”. Yeah, that is a terribly wrong explanation. Only people who do not care about numbers can say that kind of shitty thing (they should be in a toilet, flush it). In 2004, coca-cola, Hershey’s, and Pepsi, those sweets company’s revenue did not reduce, on the contrary, they increased. As a story, “carb craze hitting” is easily believable, but there is always a lie in the simplest the most understandable story.

Another explanation for the sales drop in 2004 (ending Jan 2005) was that Krispy opened too many stores and sold too many donuts in supermarkets, causing cannibalism. But think about it, there were only 300-400 Krispy shops in the US, so how did the newly opened 30 stores in fiscal 2004 cause that trouble, while 28,000 Dunkin Donuts stores in the US didn’t cause that problem?

Here is the conclusion: Krispy’s sales suddenly dropped, because the financial statements were made up since 2000’s IPO, and in 2004 the true figure was finally revealed.

We had to get the indication of fraud from 2003’s (ending Feb 2004) Financial Statements. In 2004 the stock dropped from $38 to $10 (74% drop!) in a year. this radical drop was enough to ruin investors’ lives. Investors must detect that before that happens.

Here are the indications of Krispy’s accounting fraud.

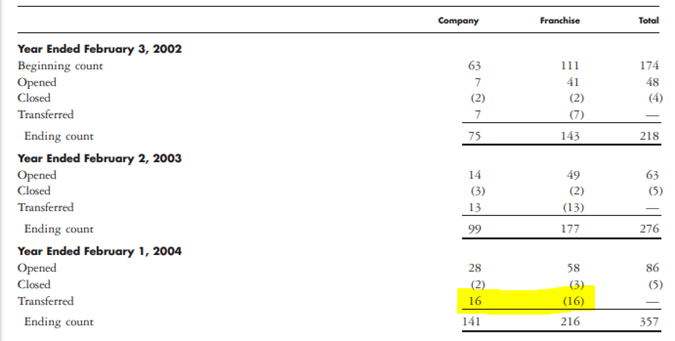

1: Why they were buying their franchisee’s store, that is WEIRD!

Franchise business is great. I mean franchisees are the ones who are screwed, not franchisers. McDonald’s one of the most profitable businesses in the world (net profit margin 34%!) gets that profit because franchisees own the risk instead of McDonald’s. McDonald’s charges franchisees a 5% to 6% fee based on their sales, regardless of whether the business is successful or not. Even when the shop fails, McDonald’s just doesn’t incur any loss.

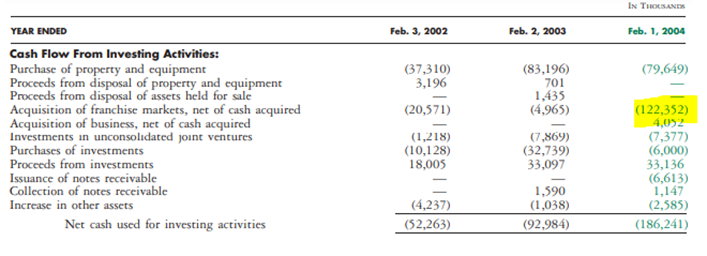

I mean franchisees are money-generating golden gooses. Why the hell does a franchiser have to kill the goose? Unthinkable. If a franchisee wants to own stores, why don’t they just build a new one? They bought 16 franchisee stores in 2004. The price was crazy $122 million (from the 2003 annual report)

evidence

the shop numbers

Cash flow statement

That means they bought each store for 7.6 Million. That is way more expensive than opening a new one. This is wrong, apparently fraud. No one wants old shops with that crazy price unless they are got-brain-transplant-with-a-mouse kind of stupid. From the cash flow statement above, the store opening investment was 79.6 Million, and the number of new stores opened (not bought from franchisees) in February 2004 was 28. Each price was calculated as $2.8 Million. This investment is also highly doubtful because it is still too expensive, but if they built only big flag shops like donut factories, this is possible.

Also, compared to other year’s franchise acquisition prices, the Feb 2004’s franchise acquisition costs were way more expensive,(in Feb 2003 it was only $ 5 million for 13 franchise stores, each costs only $380,000 (which is believable for old dingy stores) in Feb 2002, they paid $20 Million for 7 stores(that must be faking fraud, too expensive for normal old stores))

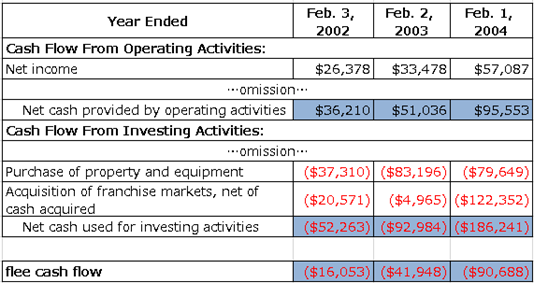

2: Free Cash Flow has always been negative since the IPO even though the net incomes were positive

Normally when doing business, your intention is to generate cash, right? However, Krispy’s free cash flow figures were consistently negative.

You can easily calculate free cash flow from the cash flow statement. Free cash flow equals net operating cash flow minus net investing cash outflow.

Operating cash flow is crucial as it shows whether you can generate cash from your business operations. If it’s negative, it indicates a serious problem that should be addressed immediately by turning it positive.

Free cash flow is literally the cash you can use freely. You earn cash from operations, spend it on necessary investments, and what remains is your free cash flow.

Companies can use free cash flow in various ways: paying dividends, repaying debt, holding onto the cash, or even making questionable decisions like gambling or buying millions of donuts to burn for no reason. It’s truly discretionary money.

Therefore, you should focus only on the blue sections of the cash flow statement and ignore the rest.

Cash flow statement

The goal of all companies is to maximize free cash flow, which is also the only natural source of cash for investment. While you can borrow money to invest, you have to repay it. This often leads to a cash crunch, which is the most common cause of bankruptcy. However, if you use free cash flow, you don’t have to repay it.

A company wants to use it wisely. Don’t want to make it negative unless the investment is truly important to acquire cash flow in the future. Negative free cash flow does not always indicate it is a fraud for example, growing companies sometimes need big investments to expand their revenue. But you have to be very careful when you observe perpetual negative free cash flow. In this case, the net profit can be fake.

The following is just my guess. I was not a Krispy Kreme auditor who could check the company directly, so the truth was never known to me.

I think Krispy was a fraud genius. They accounted for fake sales, but the cash never came because it was fake sales. When the sales cash isn’t paid, the amount becomes receivables on Balance Sheet.

So, normal fraud companies just keep piling up the receivables that will never be paid. This is easy to detect. Because the receivables/sales ratio increases so rapidly, the fraud becomes obvious.

But Krispy instead of accumulating receivables, they used franchise acquisition to fake sales cash receipts. I mean, we saw it purchased franchisees’ shops at crazy expensive prices for no reason, this is a key to recognizing the accounting fraud.

They exaggerated sales figures since the IPO, but they can’t get paid for the fake sales. So, Krispy pretended to pay a lot for franchise stores. But these payments were fake—they didn’t have no intention to give that money to franchisees. Then Krispy retrieved their overpaid cash from the franchisees and pretended it was a receipt from their clients for the fake sales so that they could reduce the receivable amount.

In an accounting system, you can’t reduce the amount of receivable without getting payment from your clients.

The made-up accounting is like this.

receivable 100/sales 100

franchisee assets 100/cash 100

cash 100/receivable 100

I think the sudden disappointing fiscal 2004’s (ending Jan 2005) figure is true one and in fiscal 2005 the sales and profit dropped further because they got the very bad impression, nobody wants to eat the donut.

When failing to use a USP…

Krispy has a great USP (unique selling proposition), and everybody says Krispy is way better than rival Dunkin Donuts. But how come the strength doesn’t show up on financials? Why has it always made losses?

See the USP of Krispy Kreme

Target: Women who like cute, sweet things. They often show up in a café, with their friends or date.

Problem: They lack happy hormones in the brain, making them sad and unhappy. At that time, they wanna eat sweet things to enhance their mood.

Eating a normal donut is also problematic. It is dense and they can’t feel sugar, because sugar is spread all over the dough. It contains a lot of sugar but still doesn’t taste sugar much. It feels like a betrayal. They can’t be satisfied with one, so eat multiple. The huge dough absorbs a lot of oil, making it unhealthy.

Ideal situation: They want to have a happy sensation of eating a lot of sweets, but actual sugar and fat intake are not that much.

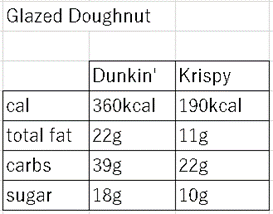

USP: Krispy Kreme donuts are airy. So, the dough part doesn’t contain much sugar. When they eat the donut they feel sugar directly from the thick sugar coating (glazer) all over the donut. The sensor on their tongue directly senses the sugar, releasing happy hormones inside their brain.

Krispy’s donuts do contain much less sugar, making the donut kinda bonus to anyone on a diet.

Let’s see nutrition facts. The same glazed donuts. It is amazing, everything Krispy’s Donuts contains is half. But giving more satisfaction. Which one do you choose?

Sources: https://www.youtube.com/watch?v=9CI6PSiHR1I&t=521s&ab_channel=InsiderFood

This USP seems to totally work, right? The donut price of Krispy and Dunkin’ depends on location, but people generally think Krispy’s price is slightly higher than Dunkin’s.

But Krispy is not profitable, a loss-making company. How that can happen if they have a great USP? This indicates their price is not high enough.

People don’t know about Krispy Donuts’ low curb advantage because Krispy doesn’t seem to focus on the fact and advertise it. Focus on your USP Krispy!

They can’t raise their prices way higher than rivals because there are so many substitutions. You have to think about this: if the company suddenly disappears from the earth, who will suffer? Do they feel at a loss? If Krispy suddenly shuts all shops down, that certainly makes American people sad, but then they just go to a supermarket and buy candies and chocolates which condense sugar in tiny portions, giving them direct sugar shock, making themselves happy again. They already forget about Krispy in the afternoon.

This happens when customers don’t recognize your product’s advantages.