Magic Trick Revealed: elf’s Secret Of Awesome Sales Surge

elf is a cosmetics maker in the US. It sells high-quality cosmetics (no animal cruelty 100% vegan) at a very cheap price that no other company can match. Many product’s prices are more than 70% cheaper than competitors’ products. Who doesn’t want it? (maybe some dudes)

The company’s stock kept going up and PER (price earning ratio) reached 90 in Feb 2024. PER is calculated by share price/net profit per share. If it is high, its net profit is expected to glow a lot in the future. The stock was traded at a very high price.

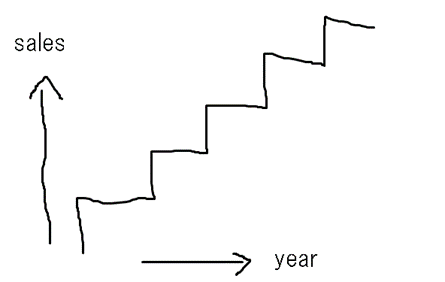

This is because their sales increase very fast and the pattern is stable stair shape, which is a very important factor for high stock valuation. Investors hate irregularity. Stable rapid growth is golden. Also, the company is generating tons of cash, not only profit. I will explain the very important difference between cash and profit.

Anyway, to see what makes it grow fast, let’s look at their USP (unique selling proposition) first. If you don’t know how to analyze USP please read my Toy’s”R”Us article.

Target: young women, who love cheap things, and they are into beauty. They are young, so they do not have money a lot. But they don’t want to compromise to use low-quality cheap cosmetics. They are heavy users of SNS. They especially like TikTok.

The ideal situation for a target: the cosmetics are very cheap, so they can save money. They can use the money left over for tasty food or a good place to live. They have no worries about the cosmetics on their skin that they use every day because they know it is very safe. Also, it makes them very cute, everyone from TikTok says this makes them the cutest. I mean, skin becomes smoother and brighter. Fixing makeup takes time, so it should last all day.

Problems: good cosmetics are expensive. Like a foundation from a well-known cosmetic maker costs $90. And that is not the only thing they need, they have to buy many other cosmetics.

There are independent cosmetic brands selling cheap, but consumers don’t know which is safe, and which is good before they actually try it. There is a high risk that it can be a waste of their money.

elf’s solution: high-quality cosmetics from a very famous trustful brand which is also cheap.

Their products are very cheap because these all made in China. So, it is selling way cheaper than those rival makers still making a profit. elf’s cost of revenue rate has been around 33% of the sales amount. For Estee, it was 29% in 2023. Estee is selling products at premium prices, but the cost of sales rates of both companies were almost the same. This is because only elf’s product is made in China, even selling price is cheap, the purchasing price from China is way cheaper. For example, Estee’s subsidiary MAC is selling a concealer for $30, and elf is selling one for $7. It is retail price, so manufacturer prices may be $15 and $5. The cost for Estee may be $4.5, and $1.6 for elf.

elf’s net profit rate(net profit÷sales) for 2023 was 10.6%. this is very high in the makeup industry. Other big competitors Coty 8.9%, and Estée Lauder 6.3% even though they are selling products at premium prices. To sell expensive makeup, they have to spend heavily on advertising to build their brand image.

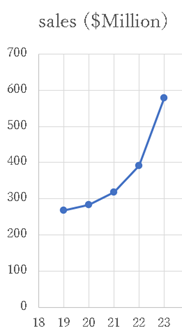

The sales for Estee were $16B (billion) in 2023, and for elf, it was only $580M (million). Estee’s sales were 30 times bigger than elf’s, but the net profit rate was smaller than elf’s.

Don’t you think this is weird? When a company sells more, economies of scale kick in, so profit rates become higher. That doesn’t happen in the makeup industry, I explain why.

These days makeup companies don’t have their own factories. They are outsourcing the production. elf is outsourcing production too. That makes its ROA high. ROA is calculated by net income÷total assets. When the denominator is small (light assets), ROA becomes higher. ROA shows how the company uses its assets efficiently. elf’s ROA was 10% in 2023, for Estee it was 11.4% in 2022.

When a company doesn’t have its own factory, and just purchases products from outsourcers, increased sales volume doesn’t reduce costs.

Economies of scale are about fixed costs per product reducing as sales volume increases. For example, if you rent a shop for $1,000, it is a fixed cost because it is the same even if you sell 10 products or 1,000 products. And if you sell 10 products, the fixed cost per product is $100, but if you sell 1,000, it becomes only $1. It is the magic of economies of scale.

Normally, factories are fixed costs, so when they increase production, the cost is reduced. But those companies don’t have it, can’t get the effect.

You may think “But Estee is bulk buying products, so they must get a significant discount”, not exactly. Estee owns many brands from MAC to TOM FORD, so they have to purchase diverse products from outsourcers. In that case, those outsourcers can’t bring the production cost down because it is making diverse products. That is why the Estee can’t get the bulk buying discount either.

That is why even a small company can compete with the biggest company in this industry on price.

The company’s sales have increased so rapidly, because of the cheap price and the good quality. Especially in 2022 and 2023, the growth accelerated.

I found that the biggest hit products of elf have been released in those years. Those products are often called “Dupe”(duplicated). elf’s best hits products have in many cases very similar predecessors’. Dupe products are like:

・The ELF Power Grip Primer$10 was released on December 18, 2021.

It is very similar to Milk Hydro Grip Primer $34 launched on March 8, 2019.

・The ELF Halo Glow Liquid Filter $14 was later released on July 17, 2022.

It is very similar to Charlotte Tilbury Hollywood Flawless Filter $44 released on April 10, 2018.

・The ELF Camo Hydrating CC Cream $14 was later released on December 24, 2020. It is very similar to IT Cosmetics CC Cream $40 released first in 2013.

elf is selling these at dumping prices. And these product’s quality is very good, sometimes better than the original ones. That is why I say elf is like a Chinese super-counterfeit goods seller. They imitate great products and sell them at very cheap prices.

They can get infinite product ideas from the cosmetic market. They don’t have to invent great products just imitate them. The product sells itself. elfing genius!

But this dupe strategy is also very necessary for elf, since it is outsourcing to China. I mean, it takes a very long time from development to production in China like 6 months, unlike outsourcing to a local company.

To significantly lower the price, they have to narrow down the product line and produce a lot of the same product to get a bulk buy discount. Additionally, making changes after products are already in production is not easy.

Therefore, in this case, they can’t afford to experiment with their original new products, repeating minor changes. They must be certain about the product’s success before outsourcing it to China.

This strategy seems working for elf, but I always say being cheap is the worst USP (unique selling proposition) and not even a USP. USP aims to raise prices, boost gross profit, improve net profit rates, and secure future cash flow. Lowering the price is exactly the opposite of the objective.

But for elf, the USP being cheap is OK. Because it is earning a pretty high gross margin. And in this industry economies of scale don’t apply, so it is less likely for a price war to break out due to increased scale.

Still, using low prices as a USP is risky. And anyone can emulate elf’s strategy. Just find great products from a market imitate them and outsource it to China.

Now the company is very OK because there are no strong competitors. But in the future, there is always competition. Once strong competitors show up, the situation can change radically. If they also use low prices as a USP, a price war occurs. They may end up lowering prices to a very unprofitable level.

When the situation changes, the company has to change its USP anyway. If they can’t evolve, they go bankrupt like Toys”R”Us. Making a new USP takes time, so they have to prepare for it early on.

The company’s growing fast thanks to the USP. But the important thing is, when a company’s sales increase, cash often reduces. This is counterintuitive, but almost all growth companies experience cash shortages during its growth. Because the company has to put more cash into operation as sales grow. For example, Company A’s inventory is $50, sales are $100 and profit is $10. When sales increase to twice ($200), inventory often increases at the same rate, so in this case, to $100 and the profit becomes $20. But cash flow is $20-$50=-$30 because you have to put $50 more cash into inventory leading to negative cash flow even though profit increases.

To see how sales increase impacts cash flow, you should check the CCC (Cash Conversion Cycle). CCC shows how many days it takes to turn its inventory into cash. If you don’t know what CCC is, please read my article.

CCC is equivalent to the number of months of sales cash required for operation. For example, when yearly sales are 120 and CCC is 1 month, the cash required for operation is 1-month sales amount which is 120×(1 month/12 months)=10.

For elf, CCC in 2023 was 2.4 months. That means when they increase sales twice, they have to put in additional cash that is equivalent to 2.4 months of sales.

For example, in 2023, sales were $580M (million), so if it becomes twice the size by adding another $580M in sales, they have to put additional cash of $116M (580M×2.4/12 months) into operation.

Since the net profit rate for the company is around 10%, so profit may increase by $58M but the operation cash payment -$116M so the cash decreases by $-58M when that happens theoretically.

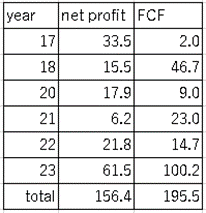

But still, the company has always made free cash flow exceed accumulated net profit in the past as you can see below. FCF (free cash flow) is net operating cash flow plus net investing cash flow. This is because of stock-based compensation. Giving stock options to employees doesn’t require any cash outflow but it becomes a cost of the company. For example, if you issue $10 worth of stock options to an employee, it is a cost, so the net profit is -$10. But you do not pay anything, so you add the $10 to the net profit to make cash flow $0.

from financial statements of elf

The company is generating more cash than net profit, even though it is growing very fast. That is very rare.

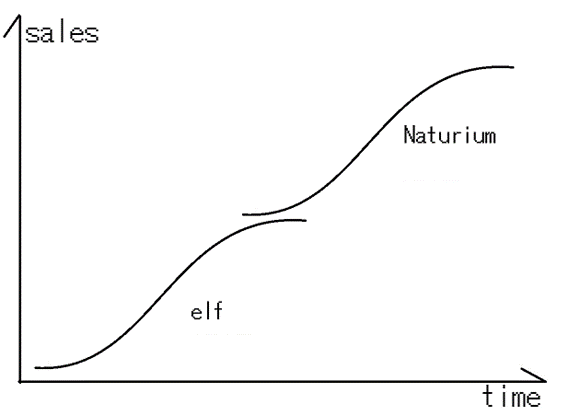

Naturium: To Buy or Not to Buy

Companies have to invest their cash to acquire further cash flow in the future. elf doesn’t just pile up the cash; they invested big in buying out a company: Naturium.

In August 2023, it bought the fast-growing skincare company Naturium. Great quality, cheap, and growing fast, it is like another elf. Those two companies’ cultures must match very well.

They paid $350 million with $200 million debt. Naturium’s expected net profit in March 2024 was still only $4 million, and its PER (price-to-earnings ratio) is almost 90, very high. The most important factor when purchasing a company is affordability. Cheap is good; expensive is bad.

elf executives must think like this: Naturium’s high growth justifies the price. They think Naturium will continue growing at a high speed in the future. It is like they bought an earlier version of elf for only $350 million. Compared to elf’s market value of $11 billion in February 2024, it is crazy cheap.

That is correct if Naturium keeps increasing its sales at a rapid pace in the future. Nobody knows the result right now.

The best situation for elf is they use piled-up cash from the operation to buy a company, and they don’t have to borrow cash or don’t have to issue new stock.

Even though elf is cash-rich, they didn’t have $350 million, the price for Naturium. So they issued new stocks and borrowed $200 million. That was almost a Leveraged Buyout (LBO) since the debt rate in the payment was high. An LBO is buying a company using borrowed money. The investment company that bought Toys”R”Us failed big because they borrowed too much money, and the interest cost severely pressured net profit.

From the December 2023 quarterly report, the interest rate was 6.7%. They have to pay an additional $13 million each year. But unlike Toys”R”Us, the $13 million is only 10% of elf’s March 2024 net profit of $127 million. The interest cost is not a big problem.

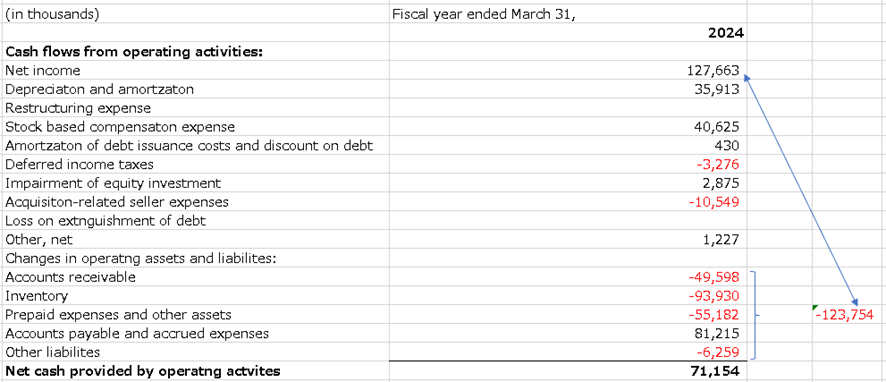

However, when I see the Cash Flow statement from the 2024 annual report, the cash outflow from operation is almost the same amount as net income.

This is because when sales increase, they have to put more cash into operation (for example, when sales increase, inventory also increases, and they have to put more cash into inventory, causing the cash to decrease), and the amount is equivalent to net income. Additionally, the company has to pay the debt it borrowed. The company is not in a dangerous zone, but a mild cash crunch is expected in the future.

The good thing about Naturium is that its sales of around $100 million are only one-tenth of elf’s sales of $1 billion. So even if Naturium increases its sales twice every year, the increased operating cash need is only a tiny portion compared to elf’s size, and elf will generate the cash (mainly from net profit) that is needed to increase Naturium’s operation without significant difficulty.

The debt amount is $260 million, and the total debt plus equity is $1.1 billion after the buyout in March 2024. The debt-to-asset ratio is only 23%, which is not a high rate. This company seems healthy. Sometimes borrowing cash and betting big is necessary, I guess.

Any business will decrease in the future, drawing an S-curve, but maybe Naturium will draw a new S-curve in the future, keeping the company growing.