4 Important Lessons to Cut Inventory and Get More Cash

Reducing inventory in your small business brings many benefits. For instance, increasing profit and cash flow. Profit increases by maintaining a minimal inventory, as you avoid selling items at a discount or discarding unsold products.

Cash flow improves because your money isn’t tied up in excess inventory. When you have large inventories, your cash remains locked in products. Increasing sales typically requires more inventory, which means more cash invested in stock. By reducing inventory, you can free up cash and make it easier to expand your business.

Today, I want to explain how to reduce inventory using Dell as an example. Dell is known for cutting inventory to the bone, and this strategy helped build a $100B empire.

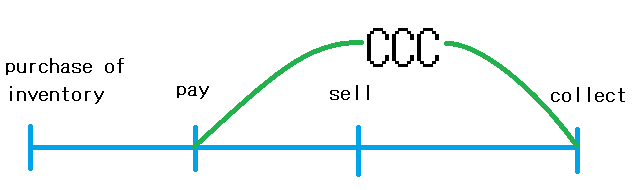

The secret to Dell’s rapid expansion without acquiring huge debt (almost no debt) is its negative Cash Conversion Cycle (CCC). CCC is the period from when a company pays for inventory purchases to when it sells the product and collects payment from the customer.

Why does this matter? Because this is a “no cash” period. If you pay $100 for inventory, you have no cash until you collect the sales price. The longer this period lasts, the longer your cash remains unavailable. Cash is like oil for a car—a prolonged “no cash” period creates a tough situation. The shorter this cycle, the better.

Normally when sales increase, cash decreases; this is counterintuitive but true. That’s why rapidly growing ventures often seek venture capital.

However, when the CCC is negative (yes, the CCC can be negative), you can get more cash as sales increase. This means you get paid first, then pay the inventory later. No venture capital and share dilution are needed like this.

Getting cash-rich and spending the cash for future growth is the key to a great company.

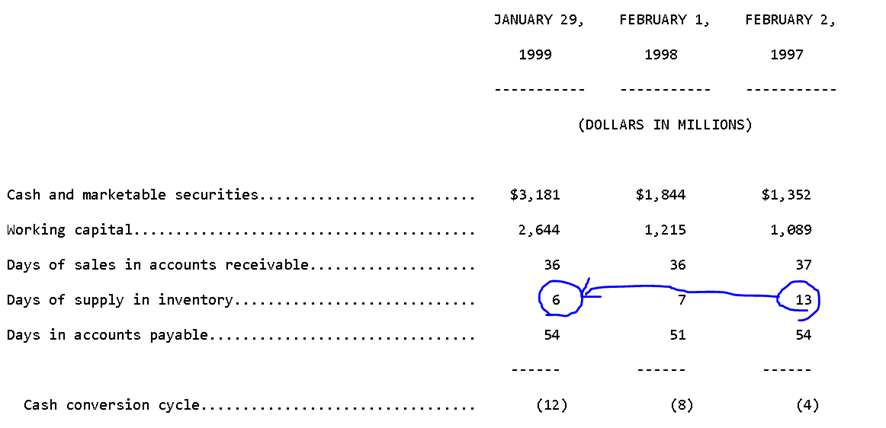

Look at the table below. This is Dell’s CCC on the annual report. Normally, companies don’t disclose this information, but Dell was the king of strong CCC, and it was an appeal point, so they disclosed it voluntarily.

From 10-K

Accounts receivable

Surprisingly, 90% of Dell’s clients consist of institutions. Even with direct selling, institutions don’t pay with cash or credit. They pay later, and it becomes receivable to Dell. Hence, DSO (period from sale to receivable collection) is 36 days.

This is short compared to rivals. In 1999, Compaq had 63 days, and HP (Hewlett-Packard) had 51 days. 36 days is short. I guess Dell used its very low price in payment term negotiations, like “our PC is very cheap, no rival company can provide at this price, so pay the bill faster!”

If you’re providing truly unique value to customers, you can use it in negotiations too.

And of course, its direct sales (not retail sales) model contributed to short DSO. Dell gets paid with cash or credit immediately from individual customers.

By the way if If you want to know more about CCC, please read my CCC article

Accounts payable

The DPO (the period from product purchase to payment) is long. Rivals had: Compaq 41 days, HP 30 days. If Dell’s DPO was 41 days, CCC would be positive, bad (we aim for negative CCC). So let’s make it longer, but how?

Mr. Dell said in an interview, “Working with a handful of partners is one of the keys to improving quality.”

I think the reason DPO is long is because Dell works with a small number of suppliers. By offering them the opportunity to sell large volumes of parts, Dell can negotiate longer payment terms.

Also, since Dell is selling directly to customers without retailers, it’s easier to predict demand directly. And since inventory sells very fast, only short-term prediction is needed.

It’s like weather prediction. A weekly weather forecast is much more accurate than forecasting weather 3 months later.

Predictable demand is good for suppliers too. And Dell enabled suppliers to access Dell’s real-time information. Suppliers can avoid excess inventory, which is a huge advantage to suppliers.

See? Everything is about giving advantages.

Very little inventory

Inventory is the most important part. Compaq had 19 days, HP 42 days. These are low, but Dell’s 6 days was insanely low.

Not only does this make CCC negative, but having low inventory is a very important strategy to survive in the PC business.

Dell eliminated risks associated with carrying large inventories of finished goods. Unsold inventory can lead to write-offs that reduce profits. This is especially important in the PC industry, where products become outdated quickly due to rapid technological advancements. Consumers are reluctant to buy a PC when a model with twice the processing power is expected to be released within a year (this is called Moore’s Law)

The cost of microprocessors goes down too (Moore’s Law implies), so the inventory value decreases rapidly. Having a lot of inventory is very risky in the PC industry.

Why is Dell’s inventory so low?

Accurate demand prediction: As I mentioned, Dell’s demand prediction is very accurate. This reduces the excessive inventory.

Buy parts and assemble after order: Dell buys some parts and assembles after receiving an order. You don’t know which one will sell until you get an order. You can avoid dead stock of finished PCs this way. The important thing is that you can assemble the PC very fast after receiving an order.

They made the following improvements to assemble faster: ・Make PC design easy to assemble ・Reduce component parts to make it faster ・Pre-install Windows 98 ・Use fast internet cables to download necessary software faster

Also, JIT (Just-In-Time) reduced inventory significantly. JIT means receiving only the amount a company needs each time, and the suppliers deliver goods crazy frequently, like every 2 hours.

The advantage for a JIT-adopting company is that they reduce inventory significantly and avoid having dead stock remaining forever on the shelf.

For example, if a company sells 365 units a year (cost $365), and if they receive goods only twice a year, the company first pays $182 to have the inventory. This means you first need capital of at least $182, then your cash will stay in the inventory for at least the next 6 months until it is retrieved after the company sells it and collects the receivable.

If you adopt JIT and purchase and receive each time you need it, you only purchase $1 each day and sell it. The necessary capital is only $1. You purchase it, sell it, collect the cash, and reuse the cash to purchase the next goods, repeating this cycle. You don’t have to make your cash stay as inventory; you can invest your cash in other things like sales or marketing.

And since you have only $1 in inventory each time, dead stock risk is minimal. If you have stock of $182, when the majority becomes dead stock, it would be disastrous.

However, buying huge amounts at once often gives great discounts. If you have enough cash and you predict there will be very little dead stock, maybe it’s a better choice to buy in bulk.

But if you need more cash, you have to keep inventory low, JIT is ideal.

Dell’s JIT was kind of extreme:

- Suppliers must have their warehouse within 15 minutes of Dell’s factory

- Suppliers must deliver a minimum of every 2 hours

Suppliers accept these radical conditions because Dell limits its suppliers, Dell will buy a lot from suppliers, and demand is predictable. It’s a great deal.

While JIT is for big companies that can buy huge amounts with purchasing power, small companies can also use the concept. Getting deliveries as frequently as possible, each time with a small amount of items, will give you great advantages too.

The JIT concept can be applied to other things. You pay for sales or marketing on performance; you buy the service as you get sales and collect cash. You pay the commission or fee by installments, not at once. Or you can avoid annual subscriptions for services.

What went wrong with Dell?

Dell is a great company focusing on hardware business operations, making it the most efficient business. But it failed to invest the cash in new innovation to create future cash flow.

Sales decreased after Chinese and Taiwanese companies entered the industry and sold cheaper PCs than Dell. Dell’s strong point was only pricing, but nobody can beat China on price.

This is a typical innovator’s dilemma. Here’s what happened to Dell: Dell wanted to invest the cash cleverly, but other than hardware, Dell didn’t know if it would be profitable or not, and many times it was very unprofitable. So they thought don’t invest in innovation, just invest in operations or no investment is suitable.

They only realized the need for innovation and investment for future cash flow after the Chinese invasion happened. Before 2005, R&D spending was only around 1% of its sales, cash just piled up. It was a cash allocation disaster.

The result was a stock price plunge from $40 in 2005 to $13 in 2013. The price was so low that Mr. Dell bought out Dell’s stock and made it a private company.

But after that, Dell’s investments finally succeeded. The company went public again in 2018, and its new business in cloud computing is very successful.

even with little bit mistake of the cash alocation the genius inventory and CCC strategy made him 10th richest person.

Reference

・The Power of Virtual Integration: An Interview with Dell Computer’s Michael Dell by Joan Magretta

・Refining and Extending the Business Model with Information Technology: Dell Computer Corporation

Authors Kraemer, Kenneth L Dedrick, Jason Yamashiro, Sandra https://escholarship.org/content/qt7vn6n4z3/qt7vn6n4z3.pdf