How to Make a Simple Cash Flow Plan to Protect Your Small Business From a Painful Cash Crunch

Running a business without a cash flow plan is like driving blindfolded – you never know when you might crash. In this guide, I’ll walk you through creating a simple but effective cash flow plan in just 60 minutes. This could be the most important hour you spend on your business this week.

Why Cash Flow Planning Is Critical for Your Business

I will explain how to make a simple cash flow plan step by step. If you don’t plan cash flow, you can be easily caught in a cash crunch that will immediately finish your business. When it comes to payment, timing is the key. Think about this common scenario: in 1 more week, you can get sales cash from clients, but you have to pay the debt this week, and you are short of cash. If you can’t prepare the cash somehow, your business ends – it’s that simple.

To avoid that nightmare scenario, you have to make a cash flow plan, even a simple one, effective.

The True Goal of Business: Future Cash Flow

As I always say, the goal of business is to increase not sales or profit but future cash flow. This appears most clearly in the fact that companies are valued based on total future cash flow (which is called discounted cash flow).

Think of it as a virtuous cycle: you earn cash and invest the cash in the business that brings more cash in the future, then get the cash, invest, and repeat the cycle. This brings the most healthy business growth. With a cash flow plan, you can easily see how much you spend to grow business. Without a plan, there’s no strategy for growth – just random, capricious decisions.

What Does a Cash Flow Plan Look Like?

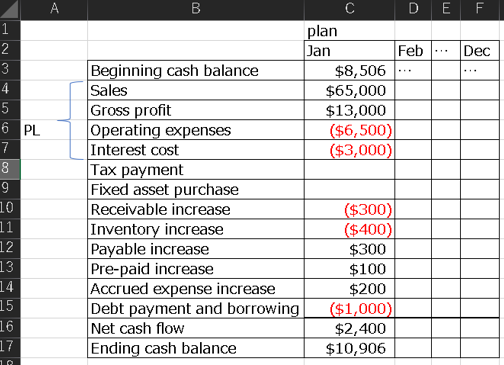

It’s simpler than you might think! You can easily make this on a spreadsheet like Excel. You’ll fill in planned numbers for all 12 months starting from this month. Let me show you exactly how to do it.

Here, you can download an Excel sample.

Step-by-Step Guide to Creating Your Cash Flow Plan

1. Start with Last Month’s Numbers

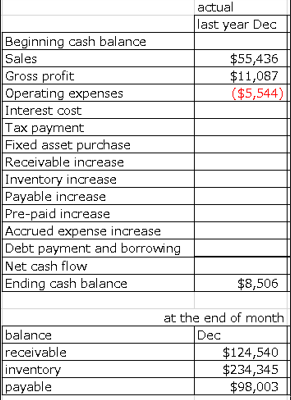

First, suppose you start in January. Begin by filling in last month’s actual figures. From Last fiscal December’s P&L (if not yet finished, you can use November’s), fill in:

- Sales

- Gross profit

- Operating expenses (to get last month’s gross profit and operating expense rate)

- Receivable inventory payable balance

- Ending cash balance

This creates your baseline for planning.

2. Predict Your Sales

This is where your expertise shines. As a professional in your business, use your knowledge of demand, marketing strategy, and other information to estimate sales as accurately as possible. Fill in sales numbers for all 12 months, making sure to consider seasonal fluctuation. This is the most important and time-consuming part, but don’t rush it – your whole plan builds on these numbers.

3. Calculate Gross Profit and Operating Expenses

Here’s where we keep it simple but effective. In the basic version, you can calculate these by just multiplying gross profit rate and operating expenses rate to sales. For example, if last year’s:

- Sales were 100

- Gross profit was 40

- Then gross profit rate was 40%

Simply multiply 40% by each month’s predicted sales number to calculate gross profit. Do the same for operating costs. Remember, operating expenses are costs, so they’ll be negative numbers.

Pro tip: If you have accounting knowledge and time, you can separate costs into fixed and variable for more precision. But for your first cash flow plan, using past rates works well enough.

4. Add Financial Costs

Fill in those numbers in the expected payment months:

- Monthly interest costs (find these in bank payment notes or contracts)

- Tax payments (calculate based on planned yearly profit)

- Fixed asset purchases (like new machinery – write these in red)

5. Handle Working Capital: Receivables, Inventory, and Payables

This part might seem tricky, but I’ll break it down simply:

When receivables and inventory increase, cash decreases because your money is tied up in these assets. When payables increase, cash increases because you’re essentially borrowing money (you owe it but haven’t paid yet).

Here’s a simple example: If you buy a book to sell for $10, and sell it for $15, but haven’t paid for the purchase yet:

- Your profit is $5

- You have all $15 in hand

- Add payable +$10 to net profit to get cash flow This shows how payable increases work.

These item amounts usually move with sales volume. For instance, if you have:

- One shop with $1,000 inventory

- Sales double with the opening of another shop

- You’ll need another $1,000 in inventory

Let’s look at a practical example of how to calculate this: When your sales increase from January $400 to February $500 (25% increase), you can easily estimate inventory by multiplying 1.25 to your January inventory of $100, which gives you $125 at the end of February. As explained earlier, the $25 increase in inventory has a -$25 impact on cash flow in February, so you would write -$25 in the February inventory cell.

You can calculate these changes for receivables, inventory, and payables using their beginning balances and each month’s predicted sales.

Important notes about seasonal changes:

- If your business has almost no seasonal fluctuation and is stable with only tiny changes, you can ignore these receivable, inventory, and payable effects

- However, seasonal sales spikes or decreases significantly affect receivables, inventory, and payables

- For strong seasonal fluctuations, manually adjust the balance of all three in those fluctuation periods

6. Consider Pre-payments and Accrued Expenses

Like payables, increases in these items affect your cash position. Write the numbers in the appropriate cells. They typically move with sales too.

If you want more details about pre-payment impacts, check my Netflix article. You can calculate pre-payment sales effects in a separate sheet and bring the numbers into your cash flow plan.

Time-saving tip: If these changes are small or very stable, you can skip this step.

7.Complete Your Plan

Finally, fill in the debt payments according to your bank contracts. Sum up all the numbers to see your net cash flow and ending balance. If any months show negative numbers, you’re in trouble – you’ll need to either borrow cash or use some of the cash flow increase strategies I discuss in my blog articles.

That’s it! The whole process shouldn’t take more than 60 minutes. You now have a working cash flow plan. Here’s what to do next:

- When you get new information, update the plan to make it more accurate

- Make a new plan once a month, always rolling forward to cover the next 12 months

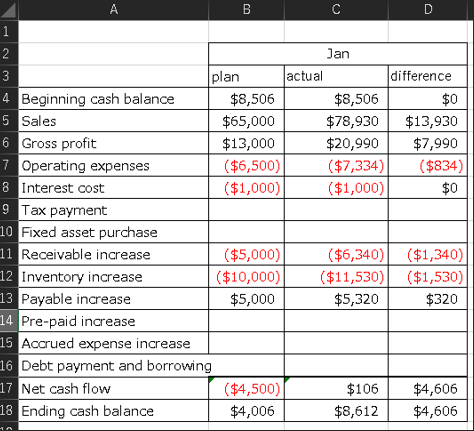

- Each month, compare your planned numbers against what actually happened

- Look at the differences between plan and reality – how different were they, and why?

- Use what you learn to make your next plan more accurate

Long-term Planning for Major Investments

If you’re planning big investments like buying new machinery or acquiring companies, you need to think bigger – make a 5-year cash flow plan. The process is basically the same, but you’ll work with yearly figures instead of monthly ones. The key point here is making absolutely sure your cash balance stays positive and you can make all your debt payments on time.

A Final Note on Accuracy

Remember – when you’re just starting with cash flow planning, getting rough numbers is fine. You don’t need to obsess over every detail. However, there’s one big exception: if your business is on the line between survival and failure, your budget needs to be much more precise. In life-or-death situations for your business, accuracy becomes crucial.