How to Get Customers to Pay Faster and Avoid Cash Crunches

I’ll explain how to speed up your payment collection schedule so you can keep plenty of cash flowing through your business and never run short again.

A business can run out of cash even when it’s generating profit. This is especially true when you’re growing — you have to invest and deliver first, and only collect cash much later.

Late payment terms like net 60 can become the single biggest bottleneck for your operations and growth.

Today I’ll explain how to speed up your payment collection schedule so you can keep plenty of cash flowing through your business and never run short again.

What we’ll cover:

- Be Unique and Essential — build negotiation power

- Payment-Beforehand Policy

- Charge More for Late Payment

- More Frequent Invoice Sending

- Yearly Payment

- Invoice Factoring

Be Unique and Essential

Making your product both unique and necessary gives you real power in payment negotiations. Your product needs to be something no other company offers — truly one of a kind.

More importantly, it must be something your clients simply cannot do without. When you nail both of these aspects, you can set payment terms with confidence.

And if your product is merely “nice to have,” clients might drop it entirely the moment you try to negotiate stricter terms. This is exactly why being unique and necessary is so crucial.

You can achieve this uniqueness by deeply understanding a specific market niche and creating solutions for their exact problems.

Also, the problem you’re solving has to be one your clients are suffering from right now — not something that might become a problem down the road. They need to be actively feeling the pain today.

To learn how to build a unique and essential product, read this article.

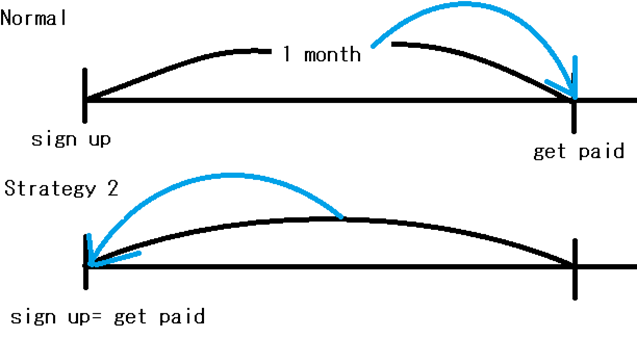

Only Accept Payment Beforehand

One of the most effective approaches — especially if you’re in B2C or selling to small businesses — is to only accept payment upfront, with no exceptions.

Once you’ve established your product as unique and necessary, requiring upfront payment becomes much easier to enforce. Without that foundation, some clients will refuse to purchase on those terms. Your negotiation power flows directly from the uniqueness and value of what you offer.

If you try negotiating upfront payment and your customer still won’t agree, move on to Strategy 3.

Charge More for Late Payment

Offer two options. Your standard policy is payment upfront — but for clients who need more time, offer late payment (such as net 30) for an additional fee.

Upfront payment is the default; late payment is the premium option that clients pay extra for.

People naturally avoid losses. When you present two options, many clients will choose to pay sooner simply to avoid the extra cost. So don’t flip this around by offering late payment as the default and giving a discount for early payment — that creates a much weaker psychological pull.

Start with Strategies 1 and 2. However, if you’re dealing with medium to enterprise-sized companies, their payment schedules are often fixed by internal policy. In those cases, you can still apply Strategy 3 — and layer on Strategies 4 and 5 as well.

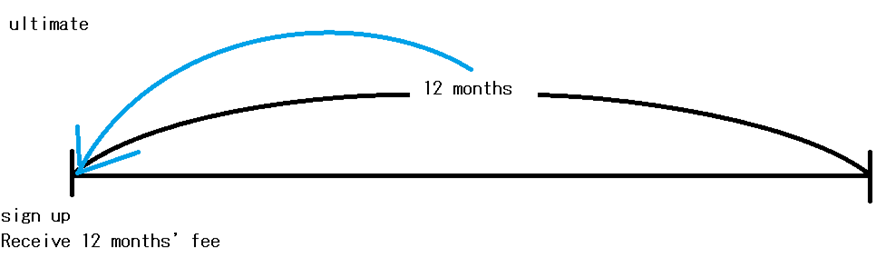

Yearly Payment

This is the best strategy of all: getting clients to pay for a full year upfront.

Larger enterprise clients often accept only late payment terms, but they are paradoxically more willing to commit to annual payment. Smaller clients may be more flexible, but rarely want to commit a full year upfront.

When your biggest customers pay annually, the relief to your cash flow is enormous — so focus your energy on persuading them first.

For pricing, set the annual plan as your default standard rate, and price the monthly plan higher as the premium option.

This makes the annual plan feel like the natural, sensible choice — clients aren’t choosing between “pay yearly for a discount” and “pay monthly normally.” They’re choosing between the standard rate and paying extra for monthly flexibility.

This logic extends beyond subscription business. If you sell a non-subscription product in a B2B context, you can still structure an annual upfront commitment — commonly called an Annual Prepaid Supply Agreement.

The buyer commits to a fixed annual spend, prepays 100% upfront, and draws down product on demand throughout the year.

In exchange, you offer benefits that make the deal attractive — for example:

- Guaranteed stock availability

- Priority fulfillment

- Fast shipping

- Annual discount

Both sides win — they get reliability and savings, you get cash in hand on day one.

Read this article on decoy pricing and annual subscription strategies to walk through how to increase your win rate when negotiating annual plans.

When negotiating an annual plan, you’ll often be expected to offer some discount. How to decide the right annual discount rate is covered in depth in this article.

Use Invoice Factoring as a Smart Pricing Strategy (Not a Desperation Move)

When you extend credit to a customer, you are effectively lending them money. A net 90 customer is borrowing your cash for 90 days — and like any loan, that has a cost. The mistake many businesses make is absorbing that cost silently instead of pricing it in.

Invoice factoring is what makes this manageable at scale. Rather than tying up your own working capital while waiting for long-dated invoices to clear, you sell those invoices to a third party (called a factor) and receive cash within 24–48 hours. The factoring fee is simply the cost of capital, no different in principle from interest on a bank loan — it just needs to be built into your pricing from the start.

Think of it this way: if your annualized factoring rate is 40%, factoring a 90-day invoice costs you roughly 10% of the invoice value. So set your price 10% higher for net 90 customers — that way the customer, not you, is paying the financing cost. And since longer payment terms also mean higher risk of bad debt, add a risk premium on top of that when you quote the price. The longer the terms, the higher the price.

Once you run those numbers, the logic becomes clear: offering longer payment terms at a higher price can be a genuinely attractive strategy. Large customers who need 90-day terms are often willing to pay more for them. You get a bigger deal; they get the cash flow flexibility they need. Everyone wins — as long as you’ve priced it correctly.

That said, always use bank financing first if you have the borrowing capacity. A business line of credit or invoice financing facility from your bank will carry a far lower annualized rate — typically 6–15% versus 20–60% or more for factoring. If your bank offers these products, set them up before you need them. Use factoring when your borrowing capacity is tapped out or when the deal size or customer profile doesn’t fit your bank’s criteria.

When evaluating factoring providers, compare: the discount rate per 30-day period, whether fees apply to the full invoice or only the outstanding balance, and whether the arrangement is recourse (you carry the default risk) or non-recourse (the factor does). Non-recourse costs more, but it also removes the bad debt risk you were already pricing in — so factor that into your calculations.

The bottom line: receivables are a form of lending. Price them like a lender would, use the cheapest capital available, and factoring becomes a tool for winning bigger deals — not a sign that things have gone wrong.

Summary

For small businesses and consumers, upfront payment should be your default. For larger clients with fixed payment policies, charge a premium for late payment, invoice frequently to cut your wait time in half, and push hard for annual commitment from your biggest accounts. That last one is the single biggest lever for keeping cash healthy as you grow.

Cash Flow Problem?

Are you constantly waiting on payments before you can make your next move? That’s a cash flow problem, and it’s fixable.

As a cash flow specialist CPA, I diagnose exactly what’s choking your cash and build practical systems to fix it.

Book Free 10-min Expert Session